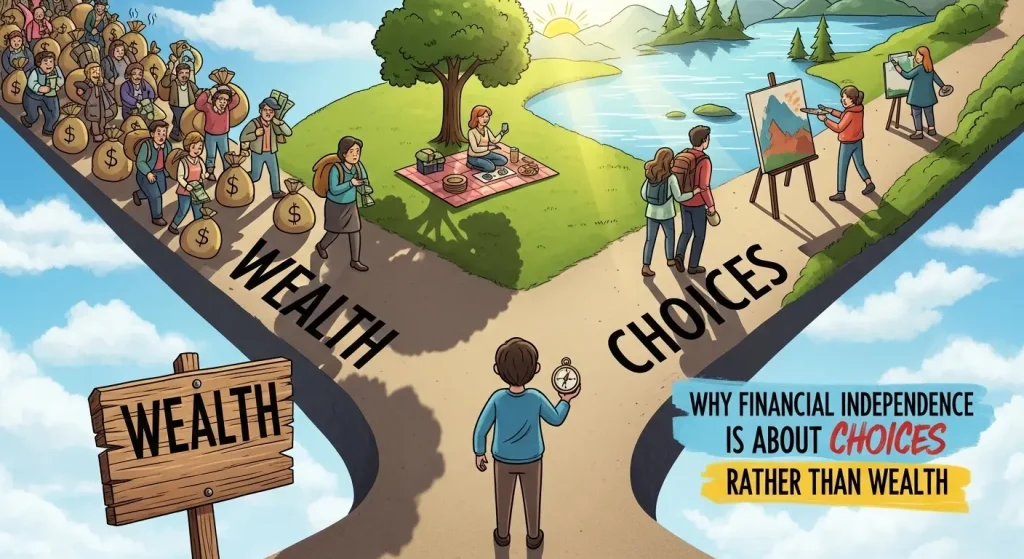

When most people hear the phrase financial independence, they picture extreme wealth. Luxury homes. Exotic vacations. Massive investment portfolios. It sounds like a finish line reserved for the ultra-rich.

But that image misses the point.

Financial independence is not about accumulating an enormous fortune. It is about gaining the freedom to choose. It is about reaching a point where your decisions are guided by your values, not by financial pressure. For some people, that shift begins after a wakeup call, maybe during a period when they relied on options like a car title loan in Kissimmee to bridge a gap. Moments like that often reveal how much stress comes from having limited choices.

True independence does not require millions. It requires alignment between your income producing assets and your living expenses. When your assets generate enough to cover your basic costs, work becomes optional rather than mandatory. That is a very different definition from simple wealth accumulation.

Freedom Is the Real Currency

At its core, financial independence is about reclaiming time. If your investments, savings, or other income streams cover housing, food, utilities, and healthcare, you gain the ability to decide how to spend your days.

That freedom might mean pursuing a passion project. It could mean spending more time with family. It might mean retiring earlier than traditional norms suggest. The goal is not excess. The goal is choice.

The Consumer Financial Protection Bureau emphasizes that financial well-being is closely tied to the ability to absorb shocks and make decisions without constant stress. Their research highlights how control and flexibility are central components of financial health. Notice the focus is not on wealth for its own sake, but on stability and control.

When you have enough recurring income to cover your needs, you no longer feel trapped by a paycheck.

Redefining What “Enough” Means

One reason people equate independence with extreme wealth is that they never define what enough looks like for them. Without a clear number tied to actual living expenses, the goal keeps expanding.

Financial independence requires clarity. Calculate your annual living costs. Include housing, transportation, food, insurance, and modest discretionary spending. Once you know that number, you can estimate how much invested capital would reasonably generate that income.

For example, many financial planners use variations of a withdrawal guideline to estimate sustainable income from investments. The Securities and Exchange Commission provides educational resources about long term investing and risk management. The principle is straightforward. Investments can produce income through dividends, interest, or growth, but planning requires realistic assumptions.

When you anchor independence to your actual expenses rather than an abstract wealth target, the goal becomes tangible.

Assets Create Options

There is a critical distinction between high income and financial independence. Someone earning a large salary may still feel financially constrained if expenses rise to match income. Without assets that generate passive income, their lifestyle depends entirely on continued work.

Assets change that equation. Rental properties, dividend producing stocks, bonds, or even a business that runs without constant oversight can provide income streams independent of your daily labor.

When assets produce enough to cover core expenses, the pressure to accept every opportunity for the sake of a paycheck diminishes. You can turn down work that conflicts with your values. You can take calculated risks without jeopardizing basic stability.

Financial independence shifts the power dynamic between you and money.

Values Over Vanity

Chasing wealth for status often leads to lifestyle inflation. Bigger homes. More expensive cars. Constant upgrades. Each increase in spending raises the threshold for independence.

If independence is defined by choice rather than prestige, spending decisions look different. You may prioritize flexibility over appearances. You might choose a modest home that allows higher savings rates. You may invest consistently rather than upgrading possessions.

This is not about deprivation. It is about intentionality. Every dollar saved and invested becomes a tool for future freedom. Every unnecessary expense that inflates your baseline pushes independence further away.

When values guide spending, independence accelerates.

The Psychological Shift

There is also a mental component to financial independence. When you know your essentials are covered by assets, your stress level changes. You approach work, negotiations, and life decisions with more confidence.

You are no longer making choices out of fear of missing a payment. You are making choices based on preference. That psychological shift can be as powerful as the financial one.

It encourages long term thinking. It supports patience in investing. It reduces impulsive decisions driven by short term pressure.

Building Independence Step by Step

Reaching independence does not happen overnight. It requires disciplined saving, thoughtful investing, and controlled spending. It also requires consistency.

Start with an emergency fund to create immediate stability. Eliminate high interest debt to free up cash flow. Increase contributions to retirement and brokerage accounts. Consider additional income streams that do not depend solely on your time.

Each step increases optionality. Even partial progress improves flexibility. You may not be fully independent yet, but each asset accumulated moves you closer to decision making freedom.

A Life Defined by Choice

Financial independence is not a trophy. It is not a flashy milestone meant to impress others. It is a quiet shift in how you experience daily life.

When assets cover your living costs, you gain something far more valuable than luxury. You gain the ability to choose your work, your pace, and your priorities. You gain the confidence to say yes to what matters and no to what does not.

Wealth can be part of the journey, but it is not the definition. The definition is choice. And when your finances support your choices rather than restrict them, you have reached the heart of financial independence.